On the heels of weaker-than-expected sales in June, U.S. dealers entered July with light-vehicle inventory at a 10-year high for the month and 8.2% above year-ago’s total.

The increase is significant because sales appear to be peaking from the six years of unprecedented growth since 2009. Accordingly, if volumes in second-half 2016 start to slide below 2015 totals, slowdowns likely are on tap for North American production and import shipments. However, such reductions could be lessened through increased price discounting, which might be necessary if the industry is to top 2015’s record sales.

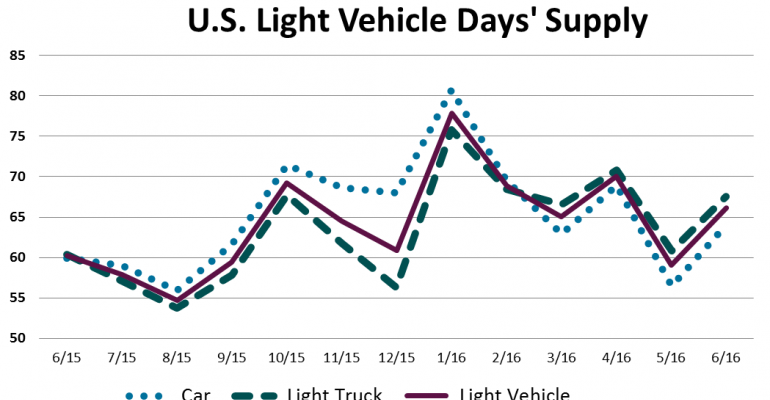

June 30 inventory totaled 3.83 million units, 1.9% above the prior month and some 290,000 units above year-ago’s 3.54 million. Days’ supply increased to 66 – also a 10-year high – from May’s 59 and same-month 2015’s 60.

A year ago, the market entered a 5-month period – July-November – when sales averaged close to an 18 million-unit SAAR. Following a normal increase in summer spiffs to help dealers get rid of excess old model-year inventory prior to ’16s coming into wide availability, the period was boosted by an atypical upward spike in retail incentives in September that helped lift sales above an 18 million SAAR in the 3-month period through November.

A similar pattern appears necessary if the industry is to avoid significant production slowdowns through the end of the year.

Sales through the first half of 2016 totaled 8.6 million units, 1.3% above January-June 2015. However, the 4-month trailing SAAR through June declined year-over-year and total volume in the period was nearly flat. A trend of relatively flat volume growth, combined with inventory more than 8% higher than year-ago, points to both slowed production and increased market incentives.

Currently, WardsAuto’s sales forecast for the year of 17.6 million units presumes there will be an increase in incentive activity to the point second-half volume matches year-ago. Without some additional goosing of incentives, sales are tracking at 17.3 million-17.4 million for the year, roughly equal to 2015’s record 17.38 million.

An indicator of whether there is a major movement in the industry to raise incentives could be how the market’s Top 3 players – General Motors, Ford and Toyota – react to a possible downturn in demand and if the rest of the industry follows.

Both GM and Toyota have been losing market share this year, including in both cars and trucks.

Using TrueCar’s ratio of average incentive spending to average transaction price, GM has lowered its incentives in the past two months, and recorded precipitous drops in market share, but kept its overall inventory in line with demand.

GM’s June stock was 2.2% below year-ago. The automaker has some car lines that could use some inventory paring and stocks of its big SUVs, with production still going gangbusters, are bordering on excess.

The bottom line is that GM has been using production adjustments more than incentives to keep inventory in balance.

Toyota’s June inventory was 9.6% above year-ago and its incentive-to-ATP ratio was up slightly during the second quarter. Despite the significant year-over-year difference, Toyota’s inventory is not heavily out of line with demand. If the automaker moves to reduce stocks, it likely will focus on cars.

In conjunction with a significant rise in incentives in 2016, Ford has reversed its market share decline of recent years. With its inventory up 18.7% year-over-year in June, the indications are Ford will continue to ensure its market share does not decline during the remainder of 2016.

Among the other major automakers, FCA’s 6-month sales share is up, as are its incentives and June inventory (6.3%).

Although still well above the industry, Nissan’s incentive/ATP ratio is down from last year, while share is up thanks to a big lift from its CUVs and vans. Inventory is less than 1% below year-ago.

With some key product refreshes, Honda’s sales were up 5.2% in the first half, with incentives in decline. Thus, its 11.2% June year-over-year increase in inventory is in sync with its demand, especially considering Honda typically has strong second-half results compared with the rest of the industry.

By vehicle type, June inventory of cars totaled 1.49 million units, 2.3% below year-ago. Days’ supply increased to 64 from the prior month’s 56 and year-ago’s 60. Light-truck stock was up 19.7% from June 2015 to 2.34 million units. June 30 days’ supply was 68, compared with May’s 61 and year-ago’s 60.

Inventory of domestically made LVs totaled 3.06 million units, up 6.7% from year-ago, and import stocks totaled 771,000, 14.8% above June 2015.