U.S. light-vehicle inventory took a healthy cut in March thanks mostly to unexpectedly high sales volume not seen for any month in several years.

Inventory was estimated by WardsAuto to be 200,000 units above optimum heading into March, but the month’s sales of 1.53 million units, highest since May 2007, chopped it to a better level.

Temporary plant shutdowns by some North American manufacturers also contributed to the streamlining.

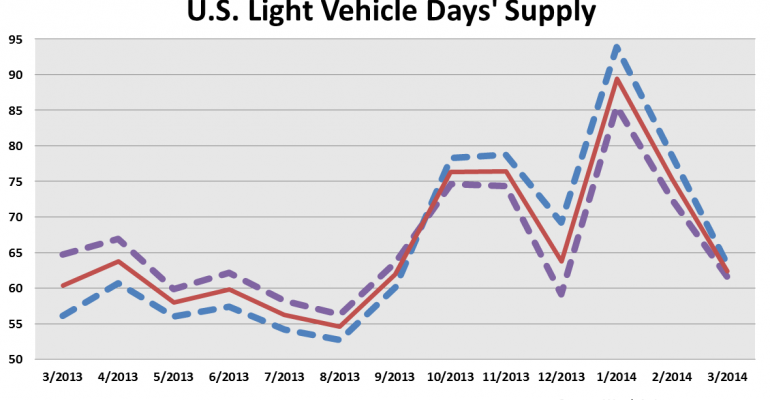

Total LV inventory, which usually either remains flat or slightly rises from February to March, declined 1.6% from the prior month to 3.67 million units, 13.3% above year-ago but equal to a 62 days’ supply, a solid level heading into the second quarter in most years.

However, taking into account that the days’ supply was calculated using March’s artificially high daily selling rate, caused by the recouping of weather-related sales losses in the previous two months, the adjusted days’ supply is 66, a little higher than optimum for the period.

Import inventory ended March at 668,251 units, 6.3% above year-ago. However, import stocks dropped 2.6% from the prior month, more than the 1.4% decline in domestically made vehicles, as March sales of overseas-built makes surged 14.1% above like-2013, compared with an 8.5% increase for domestically produced LVs.

Even though automakers are sourcing more imported models to North American plants, sales of import vehicles have increased penetration over the same year-ago period every month beginning with last July. In first-quarter 2014, imports accounted for 21.7% of LV sales compared with 21.0% a year ago.

But the month-to-month inventory decline in March does not mean the string of sales share increases for imports will end in April.

Sales of luxury vehicles are spurring imports. Although import inventory declined from February, stocks for just import luxury makes increased 14.8% over the same period. The overall decline was mostly with small cars and non-luxury CUVs. That also fits with seasonal sales trends because import luxury vehicles usually increase share in April vs. March.

Inventory of domestically made LVs is where most of the excess in overall inventory exists. There could be some production slowdowns, but it likely means higher retail incentives that were in place in March will continue in April, and possibly increase.

Furthermore, market leader General Motors’ sales should rebound in April after its market share dropped to 16.7% in March from 18.3% the prior month. GM was one of the few automakers to increase inventory month-to-month in March, but its volume of 815,492 was only 9.6% above year-ago. Major competitors Fiat-Chrysler and Ford were up 24.8% and 20.7%, respectively, with double-digit increases at Nissan and Toyota. If it becomes evident that GM is pulling in additional volume as the month progresses, its main competitors could be inclined toward more aggressive pricing.

GM’s expected bounce-back will be led by trucks. Combined inventory for its large CUVs and SUVs are up 35.0% from like-2013. In particular, GM’s redesigned ’15-model large SUVs are ready to be unleashed after sales of the older versions faded in the first quarter while the manufacturer slowed production at its Arlington, TX, plant for retooling.

Nissan’s inventory, up 16.0% from year-ago, largely is in line with its 12.4% year-over-year sales increase in March. Nissan’s first-quarter market share of 9.5% was its best-ever quarterly penetration and for the past two months it has outsold rival Honda for the No.5 slot in the U.S.

However, Nissan’s sales share nearly always drop sharply in April from the prior month while Honda’s increases. Honda was one of the few automakers to increase inventory in March from the prior month.

In April, U.S. inventory likely will decline from the prior month again, while days’ supply rises. WardsAuto estimates a 65 days’ supply on April 30 to be a healthy industry total to shoot for.