U.S. light-vehicle inventory ended July pointing to another strong month for sales in August, with demand continuing the 17 million-plus seasonally adjusted annual rate averaged over the past six months.

Inventory declined from June, which is the usual trend due to the high amount of vacation and holiday plant downtime typically scheduled for the month limiting production, but remained above year-ago’s level in line with rising demand.

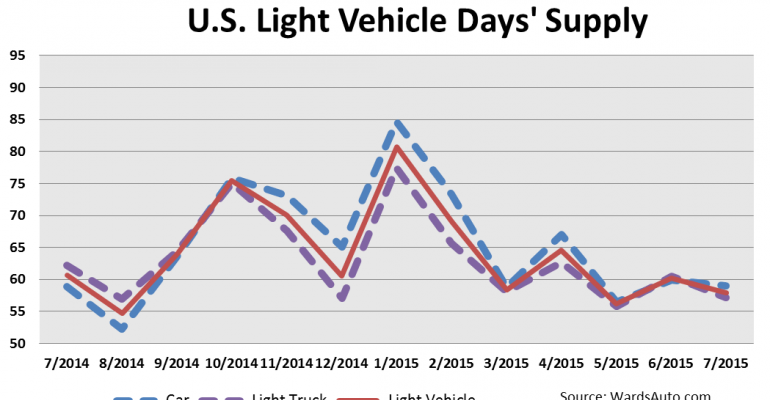

July 31 inventory totaled 3.350 million units, down 5.4% from June but 0.6% above like-2014’s 3.328 million. Days’ supply was a healthy 58, down from June’s 60 and year-ago’s 61.

As in June, the first month this year that inventory rose above like-2014, July’s increase mostly was due to more CUVs on hand, especially imports.

Inventory of domestically produced LVs declined 6% from the prior month and remained below year-ago levels by 1.5%. Volume totaled 2.697 million units and equated to a 59 days’ supply, down from the prior month’s 62 and year-ago’s 64.

However, the shortfall in domestic inventory volume and days’ supply will not necessarily translate to an upward bump in planned production. Competition from overseas-built vehicles, including CUVs, should temper demand, albeit growing, for domestics.

Import stocks totaled 653,000, 10.5% above like-2014 and 2.6% below June. Days’ supply ended at 53, same as the prior month and above year-ago’s 49.

After running below same-month year-ago totals for several months, import inventory climbed to a nearly flat year-over-year total in May and to double-digit increases in June and July. Because July’s import days’ supply remained flat with the prior month instead of falling, demand lagged the level suggested by dealer stocks. Thus, there might be an unusually high upward spike in import penetration in August from July.

CUV stocks ended July 21% above year-ago, including a 49% increase in imports and 12% for domestically produced versions. Sales penetration for CUVs is in good shape to top 30% of the market in August after doing so for the first time in July. Because CUV days’ supply was just 49, and the lowest among all segment groups, North American production and import shipments of those models will remain among the most robust of all vehicles to meet demand for the rest of the year.

Not all CUV segments necessarily will contribute to the group’s expected strong penetration in August.

Inventory of Large CUVs, a segment dominated by General Motors, was down 24% from year-ago. That follows a year-over-year sales surge in July when volume increased 22%, which was much higher than the 8% year-to-date rise through June.

Conversely, Large SUVs, after showing some weakness in recent months, could rebound in August. Inventory for the segment, also dominated by GM, is 22% above year-ago. With year-over-year sales of Large SUVs down four straight months through July, volume could pick up in August to pare some inventory and offset a temporary shortage of Large CUVs.

For the same reasons Large CUVs might post a sharp decline in penetration in August, Large Pickups could too.

July sales of Large Pickups increased 12.3% over same-month 2014, well above the year-to-date total, and share spiked upward to 12.3% from 11.2% the prior month. Inventory ended the month 19% below year-ago, with only the Ram pickup having stocks above (2.5%) year-ago.

Car inventory, with demand weak in all segment groups, ended July at 1.481 million units, 2.5% below year-ago.

Unlike the overall trend, import cars are faring worse in the market than domestics. In fact, sales of domestics are above year-ago largely due to recent sourcing changes of some vehicles to North American plants from overseas factories.

July 31 inventory of domestic cars totaled 1.125 million units, 1% below year-ago. Domestic-car days’ supply was 60, slightly below year-ago’s 62.

Import-car inventory in July was 7.3% below year-ago, with a 55 days’ supply, up from like-2014’s 52.