U.S. dealers entered September with a 12-year-high level of inventory for the second straight month, including the highest August days’ supply for cars since 1992 and import volume rising to a level not reached for the month in nearly three decades.

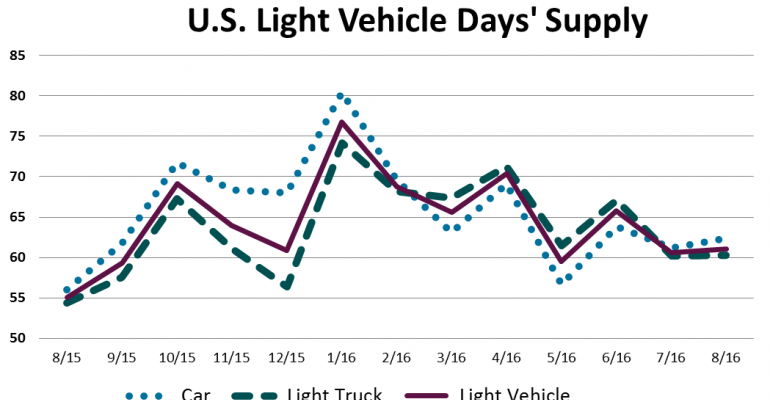

Light-vehicle inventory ended August at 3.535 million units, slightly above July’s 3.530 million and 7.1% higher than like-2015’s 3.302 million. August’s 61 days’ supply was flat with July, but well above year-ago’s 55.

August’s total was the highest for the month since 3.600 million units in 2004. At that time, year-to-date sales in the U.S., based on the seasonally adjusted annual rate, was tracking at 16.7 million units, but ended the year with volume of 16.9 million.

The to-date 2016 SAAR is 17.2 million units, same as a year ago when, similarly to 2004, volume for the entire year, at 17.4 million, ended 200,000 units higher than the 8-month SAAR. With August’s inventory this year 234,000 units above year-ago’s total, 2016’s final sales total also is expected to end higher than indicated by the 8-month SAAR.

Part of the reason for August’s stocks totaling such a long-time high is due to the month’s sales finishing below expectations. August’s 16.9 million SAAR was a sharp drop from July’s 17.7 million and 2.5% below forecast. Initial modeling for September shows a rebound to 17.4 million.

However, even if demand over the final five months rises above the 8-month SAAR, elevated inventory levels mean domestic and overseas manufacturers won’t necessarily need to raise production for the U.S. market to keep up with it.

Slowed production is expected to be mainly with cars, which, despite inventory ending August 3.7% below year-ago, still is on the high side.

Aug. 31 car days’ supply was 62, highest for the month in 24 years, and an increase from July’s 61 – significant because August days’ supply typically declines from the prior month. Inflated inventory is most acute in the entire Middle Car segment group and the Lower Luxury segment, or cars priced roughly in a range from the low $20,000s to the mid-$40,000s.

Combined sales in that range declined 21% year-over-year in August and are down 11% year-to-date, while inventory for the sector is nearly flat with a year ago. Year-to-date market share for the grouping also is well below year-ago; 19.4% vs. 21.8%, with August tanking to 18.0% from last year’s 22.1%

Conversely, sales of CUVs, the segment group mostly responsible for stealing share from cars, were up 8.0% year-to-date, with market share at 31.4% vs. year-ago’s 29.2%.

Inventory for CUVs, however, is well-balanced with demand, meaning there will not be much pressure to raise production to offset slowed car output. There even is less pressure on North American plants: Year-to-date sales of domestically produced CUVs are up 1.2%, with inventory up 18.9%, and 8-month market share (21.6%) is just slightly above last year. Import inventory is up a robust 21.4%, but sales are up a stronger 27.0%, with January-August penetration approaching 10%, compared with 7.8% a year ago.

Inventory of pickups and SUVs, which are heading into their strongest period of the year for demand, also appear well-balanced.

Combined Aug. 31 stocks of SUVs and pickups totaled 915,000 units, 14.0% above year-ago. Year-to-date sales for the two segment groups together were up 5.1%, with market share at 22.0%, vs. 21.0% a year ago.

While pickup inventories in total appear healthy, totals for the Large Pickup segment are somewhat high, though not at unmanageable levels. Boding well for the domestic production outlook is lean stock levels for Small Pickups.

Year-to-date sales of Small Pickups were up 21.1%, including a 39% rise in August. But even with Small Pickup inventory (65,000 units) nearly double year-ago, the segment is estimated by WardsAuto to be short over 20,000 units from an optimum level heading into September.

By production source, Aug. 31 inventory of domestically made LVs totaled 2.82 million units, 6.9% above year-ago. Days’ supply of 63 was an increase from year-ago’s 57 and the month’s highest since 2006.

Import inventory totaled 714,000 units, 7.6% above year-ago and highest for the month since 1987. Days’ supply was 54, up from 50 in same-month 2015.